Our enterprise infrastructure helps commercial banks, digital-first lenders, and credit unions scale loan volume and meet compliance without linearly increasing underwriting headcount.

91%

Straight-through processing rate on retail loans.

64%

Reduction in manual application effort.

65%

Decrease in contract review times.

Our enterprise infrastructure helps commercial banks, digital-first lenders, and credit unions scale loan volume and meet compliance without linearly increasing underwriting headcount.

91%

Straight-through processing rate on retail loans.

64%

Reduction in manual application effort.

65%

Decrease in contract review times.

AI delivers the highest ROI in data-heavy, heavily regulated credit and lending environments. Here is how we apply it

Automate KYC, AML, and financial data extraction directly into your LOS to instantly process applications.

Deploy localized LLMs to securely scan complex loan agreements and extract critical clauses with high accuracy.

Automatically screen incoming applications and trailing documents against regulatory frameworks and risk policies.

Instantly parse unstructured data from tax returns, pay stubs, and bank statements for faster review.

Intelligently route non-standard applications and missing document requests to the right loan officer without manual triage.

We build and deploy AI systems inside regulated financial environments where data privacy, system availability, and fair lending explainability are non-negotiable.

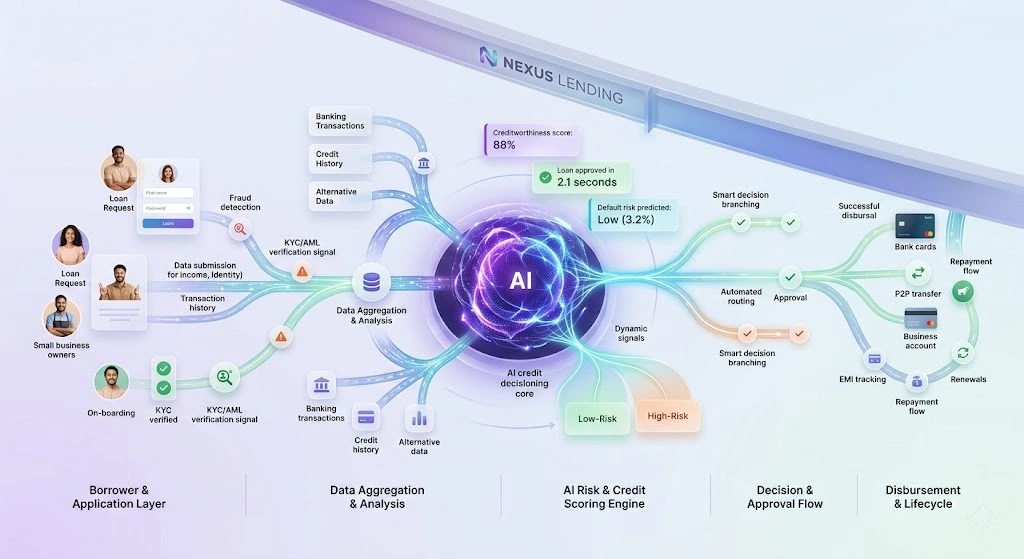

Where AI Fits in the Lending Stack

AI enhances core Loan Origination Systems (LOS) through a structured, highly secure architecture

%201.webp)

Ingestion

Pull structured credit data and unstructured applicant documents (W-2s, IDs, appraisals) from secure portals.

Secure APIs

Custom middleware connecting modern AI to core origination infrastructure like Encompass or Temenos.

Model Layer

Localized LLMs ensuring applicant Non-Public Personal Information (NPI) never leaves your secure cloud.

Human-in-the-Loop

AI handles document sorting and data extraction; final credit decisions and complex underwriting reviews route to human officers.

Common Lending Automation Challenges

.webp)

Connecting modern predictive AI to entrenched origination software requires highly specialized, fault-tolerant API middleware.

Regulators demand fully auditable logs detailing exactly why an application was flagged to prevent algorithmic bias.

Applicant financial data must remain in isolated clouds. Public AI models cannot be used for sensitive loan data.

Best Fit: Regulated banks or digital lenders processing high volumes with an existing LOS needing an intelligent modernization layer.

Not a Fit: Basic chatbots, generic document scanners, or unsecured POCs.

Best Fit: Regulated banks or digital lenders processing high volumes with an existing LOS needing an intelligent modernization layer.

Not a Fit: Basic chatbots, generic document scanners, or unsecured POCs.

Applicant document extraction, KYC/AML validation, initial contract clause review, and backend data entry into the LOS.

No. We utilize a strict Human-in-the-Loop (HITL) architecture. AI extracts and analyzes data to accelerate underwriting, but final credit approvals are made by humans.

Yes. Secure implementations utilize customized API middleware, strict role-based access controls, and localized models to maintain total NPI data security.

Front-end document extraction deploys in 8 to 12 weeks. Deep API integrations into core origination systems require longer, phased rollouts.

Our AI systems are built with transparent logging. Every automated data extraction and AI-driven workflow generates a clear audit trail for regulatory reporting.

.webp)

.webp)

.webp)

BuildNexTech empowers businesses with expert web development, app development, and cloud migration services.