UPI processes over 400 million transactions daily. The NPCI puts the success rate at 90–95% which sounds solid until you do the math. Even a 5% failure rate at that volume means tens of millions of broken transactions every month, most of them dying on weak networks or during server timeouts.

UPI Lite takes a different approach: it stores a small balance on the device itself, so routine payments don't need a live bank connection. The RBI caps it at ₹500 per transaction, ₹2,000 total wallet balance. Enough for a rickshaw, a coffee, a kirana order. Not much beyond that.

The Offline Payment Gap in India

I’ve worked closely with multiple fintech companies and even collaborated with teams at BNXT on real-world digital payments use cases. And one issue keeps coming up India’s digital payment ecosystem still struggles when the internet disappears.

Despite the massive success of UPI india and the Unified Payments Interface, there’s still a visible digital divide. In rural India, patchy internet connectivity, unreliable mobile data, and frequent transaction failures turn even simple digital transactions into a hassle.

I’ve personally faced this during travel standing at a tea stall, scanning a QR code, and waiting… only for the payment to fail. That’s when you realise most digital payment solutions are still deeply dependent on bank servers, payment switches, and the Core Banking System.

For a country pushing toward a strong digital economy, India's vision, this dependency is a real bottleneck. And this is exactly where offline payment solutions like UPI Lite step in.

What is UPI Lite and How It Works

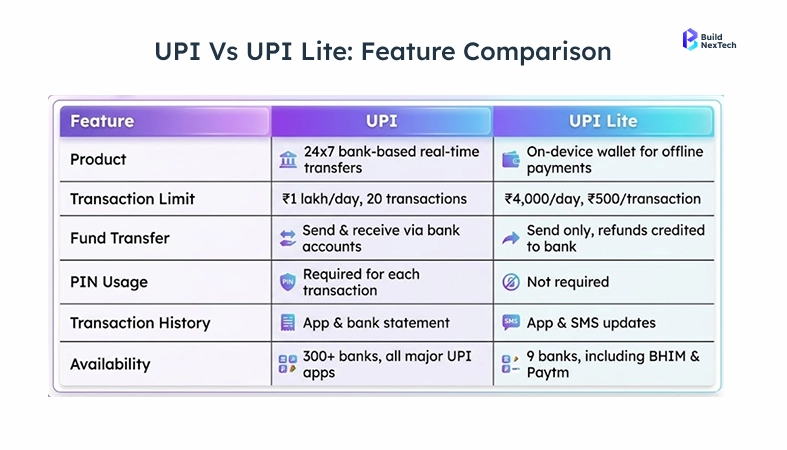

UPI Lite is an on-device wallet introduced by the National Payments Corporation of India that allows small-value transactions without real-time internet or bank server interaction.

Unlike regular UPI payments, which require constant connectivity, UPI Lite stores a limited balance on the user’s device and processes payments locally. This reduces dependency on network availability and improves transaction success rates.

.webp)

On-Device Wallet Model: How It Works

UPI Lite follows a simple store-and-sync approach, making it easier to understand and use.

Step-by-Step Flow

- Load money from a bank account into the UPI Lite wallet

- Balance is stored securely on the device

- Payments are completed instantly without contacting bank servers

- Transactions sync with the bank once the internet is available

Example Flow

Load ₹2000 → Pay ₹50 → Balance updates on device → Sync later

This model removes the need for real-time processing during every transaction. As a result, payments are faster, more reliable, and less likely to fail in low-network conditions something traditional UPI systems still struggle with.

Key Advantages of UPI Lite Over Traditional UPI

The key difference between traditional UPI and UPI Lite is reliability under real-world conditions. While standard UPI depends on network availability, UPI Lite reduces that dependency by processing transactions on the device.

What Improves

Last-mile users in semi-urban and rural regions, where network reliability directly affects whether a payment goes through at all. Daily commuters and small retail customers who make high-frequency, low-value transactions the kind where stopping to retry a failed payment is genuinely disruptive. And cash-dependent micro-economies where digital adoption has stayed low not because of reluctance, but because the infrastructure hasn't been reliable enough to trust.

Small Merchants, Transport, and Everyday Micro-Transactions

UPI Lite is most impactful in low-value, high-frequency transactions, where payment reliability matters more than complexity or transaction size. In many everyday scenarios, users simply expect a ₹20 or ₹50 payment to go through instantly something traditional UPI can struggle with in poor network conditions.

1. Street Vendors and Small Retail Shops

Small merchants operate in environments where connectivity is often inconsistent. Failed payments can lead to lost sales or a fallback to cash.

Why UPI Lite fits:

- Works without stable internet

- Reduces failed QR transactions

- Enables faster checkout for small purchases

2. Local Transport Payments (Auto, Bus, Metro)

Transport payments are time-sensitive and usually low-value. Delays or failures create friction for both users and operators.

Why UPI Lite fits:

- Instant payments without waiting for confirmation

- No need for repeated retries

- Ideal for quick, on-the-go transactions

3. Small Businesses Without POS Infrastructure

Many small businesses rely entirely on QR-based payments instead of card machines or POS systems.

Why UPI Lite fits:

- Eliminates dependency on payment hardware

- Improves reliability in low-network areas

- Supports high-frequency, low-ticket transactions

Adoption Insight

These use cases represent a significant share of India’s digital payment volume, particularly in informal and semi-formal sectors. Improving reliability in these segments directly impacts user trust, merchant adoption, and overall digital payment growth.

Security, Limits, and Regulatory Considerations

With a hard ₹2,000 wallet cap, the exposure in any compromise scenario is structurally bounded a bad actor cannot exceed what is preloaded. The more relevant question is anomaly detection: when the device syncs back online, NPCI's systems reconcile the offline transaction log against the bank ledger, and discrepancies trigger a flag before settlement completes. For disputes, NPCI's offline transaction framework routes complaints through the same grievance mechanism as standard UPI, though resolution timelines may differ given the delayed sync model. Both RBI and NPCI guidelines govern these boundaries, covering the offline framework, wallet limits, and dispute handling.

Risk Controls, Transaction Caps, and Compliance Framework

The difference between UPI Lite and conventional UPI transactions is that of security. Conventional UPI requires live bank authentication and double-checking every time a transaction is done, whereas UPI Lite operates on the stored value system and comes with a set limit, meaning there is no authentication required but still remains safe owing to controlled spending.

- Transaction limits for low-value payments

- Wallet balance caps to reduce financial exposure

- Minimal sharing of personal data during transactions

- Offline execution without dependency on third-party systems

Together, these controls create a secure yet efficient framework, enabling reliable offline payments while staying compliant with India’s regulated digital payments ecosystem.

UPI Lite vs UPI and Wallets: What Actually Changes

Unlike standard UPI, which requires an active internet connection, and digital wallets, which operate outside UPI rails entirely, UPI Lite is preloaded, natively integrated within the UPI ecosystem, and built for reliable offline transactions.

Speed, Reliability, and User Experience Comparison

The difference between UPI, UPI Lite, and digital wallets comes down to connectivity, reliability, and usage context.

- UPI (UPI payment India) → Fast and widely accepted, but fully dependent on internet connectivity

- Digital Wallets → Preloaded and usable in some offline scenarios, but fragmented across apps and ecosystems

- UPI Lite → Preloaded, integrated within UPI, and designed for reliable offline transactions

Clear Positioning

Use standard UPI for medium to high-value payments when connectivity is stable. Use UPI Lite for small, frequent payments where network reliability is uncertain. Use wallets for platform-specific cases closed-loop payments, cashbacks, or app-specific offers where UPI doesn't fit.

Role in Financial Inclusion and Cashless Growth

UPI Lite plays a direct role in financial inclusion in India’s digital payments ecosystem by reducing dependence on continuous internet connectivity. While initiatives like Digital India and UPI have expanded access, network limitations still restrict usage in many regions.

Current Challenges Slowing UPI Lite Adoption

Awareness, Device Compatibility, and Usage Limits

Even with all the benefits, I’ve seen adoption challenges:

- Many users are still unaware of UPI Lite and NPCI (National Payments Corporation of India), the organization that manages India’s digital payments infrastructure.

- Partial integration within the fintech ecosystem

- Device and smartphone penetration gaps

Also, wallet limits restrict broader usage beyond micro-payments.

How UPI Lite is Shaping the Future of Offline Payments in India

Expansion Opportunities and Emerging Payment Innovations

NFC integration could make tap-based payments faster for transit and retail. IoT compatibility opens up machine-to-machine payments vending, tolls, automated checkouts. The digital rupee adds a programmable layer that UPI Lite's offline architecture could work alongside naturally. Cross-border capability is further out, but the groundwork is being laid. The 5G rollout pushes all of this faster, though how quickly it reaches tier-2 and tier-3 cities will determine how much of it translates into actual usage.

What This Means for Fintechs and Businesses

Infrastructure, Testing, and Compliance Readiness

From what I’ve seen working with teams like BNXT and other fintech solution companies, building offline-ready systems isn’t simple.

You need to rethink:

- cloud-native architecture

- Offline-first payment instruments

- Testing for Offline UPI Payment System scenarios

- Integration with UPI Circle and UPI Credit

This is exactly where teams struggle and where Frugal Testing becomes critical.

I’ve seen projects get delayed simply because offline sync and reconciliation weren’t tested properly.

To handle this, fintech teams use approaches like frugal testing to validate edge cases such as network failures and partial transactions ensuring more reliable payments and fewer issues at scale.

Conclusion

UPI Lite solves a specific problem: small payments failing in low-connectivity areas. It keeps a balance on the device instead of depending on a live bank connection, which means fewer dropped transactions at kirana stores, bus stops, and anywhere network quality is unreliable.

It doesn't replace standard UPI. It handles the transactions standard UPI drops capped at ₹500 per transaction and ₹2,000 total wallet balance, so it's built strictly for everyday, low-ticket spending. Nothing beyond that.

How useful it actually becomes depends on app integration and whether users outside metros hear about it. NPCI backs the infrastructure, but awareness in tier-2 and tier-3 cities is a separate problem. For now, it works where it's supposed to. That's not nothing.

People Also Ask

Q. How do users enable UPI Lite on their mobile device?

A. Users can enable UPI Lite directly within supported UPI apps by opting in, setting a wallet balance, and completing a one-time setup process linked to their bank account.

Q. Are UPI Lite transactions visible in bank statements immediately?

A. No, transactions are recorded on the device first and appear in the bank statement only after synchronization when the internet becomes available.

Q. Can UPI Lite be used for merchant QR codes already deployed for UPI?

A. Yes, UPI Lite works with existing UPI QR codes, allowing merchants to accept payments without any additional infrastructure changes.

Q. What happens if a user switches or loses their device with UPI Lite enabled?

A. Since the balance is stored on the device, users may need to reset UPI Lite and reload funds on a new device, depending on app and bank policies.

Q. Does UPI Lite support recurring or scheduled payments?

A. No, UPI Lite is designed for instant, small-value transactions and does not support features like auto-pay or scheduled payments.

.webp)

.webp)

.webp)